Debt and Dating: Can Poor Financial Habits Keep You in the Friend Zone?

February 5, 2018

Auto Link Makes Car Buying Easier than Ever

February 20, 2018

Pitfalls of a Payday Loan

Financial Quick Fixes Come at a High Cost

Prohibited in 18 states, payday loan companies still manage to offer more than 20,000 locations across the United States, making them more common than McDonald’s restaurants. Banking on consumer desperation, these programs market their services to financially vulnerable customers. When potential borrowers encounter an unexpected money crunch, the appeal of getting instant cash with minimal qualifications seems too good to pass up. If the borrower is employed and receiving regular paychecks, that’s usually all it takes to get a loan. However, these loans traditionally charge rates of 300% annual interest (APR) or higher, saddling the already-struggling borrower with an even heavier financial burden.

Even though a payday loan is designed to be paid off when the customer receives their next paycheck, the outrageous interest charges often make it incredibly difficult to pay off the full amount. Since the average payday loan payment consumes 25-50% of a borrower’s income, the threat of default is extremely high. To avoid defaulting on the loan, many customers elect to pay only the interest charges and roll over the loan for another pay period. According to recent CFPB research, almost 4 out of 5 payday loan customers re-borrow within a month. What started as a temporary fix becomes an ongoing cycle of debt.

High-interest consumer loans: overspending over time

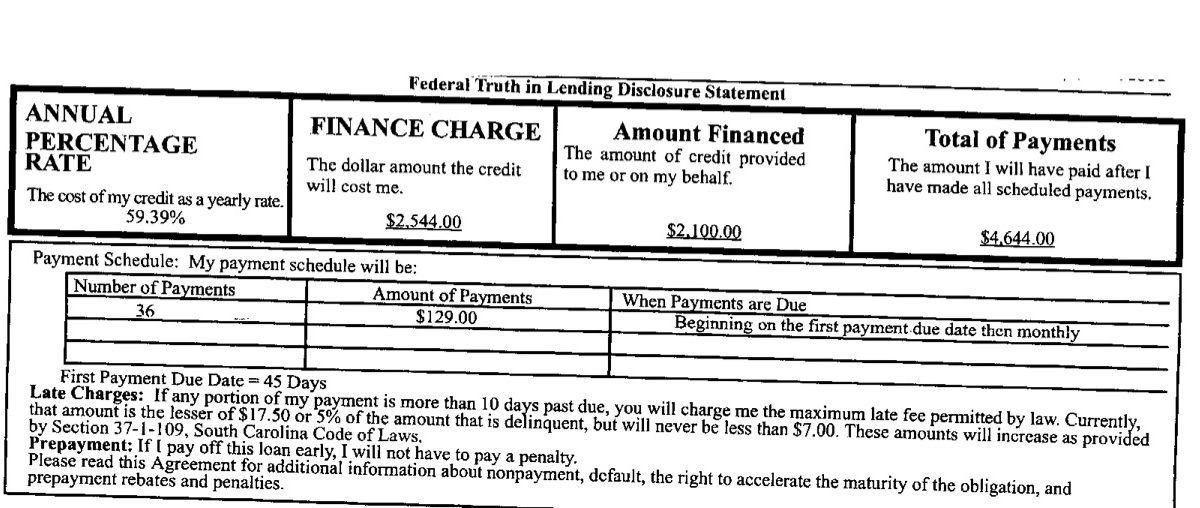

While payday lending companies are traditionally limited to loans of $1,000 or less, there is no shortage of consumer lending companies willing to offer similarly unfavorable terms on higher loan amounts. Like payday lenders, these lenders commonly target individuals with less-than-perfect credit or little to no collateral. But rather than charging outrageous interest rates for short periods, they make their money by charging slightly-less-outrageous rates (59% instead of 300%) over longer periods of time, often 2-3 years.

Consider this example (shown in the graphic above): borrowing $2,100 at an interest rate of 59.39% for 36 months would result in a total payment of $4,644, more than double the original amount borrowed. You don’t need a financial advisor to explain why that’s a bad deal. Fortunately, these lenders aren’t the only game in town.

Credit unions offer a convenient, cost-effective alternative

Because they’re structured as not-for-profit, member-owned financial collectives, credit unions are able to reinvest their earnings into programs that benefit their members—instead of paying dividends to shareholders like traditional banks. This distinction allows credit unions to approve personal loans with lower interest rates and higher flexibility than programs offered by payday lenders or banks.

For more details about how Caro can help you find smart solutions for your financial needs, stop by one of our local branches or contact us here.

{kind=link}

{kind=link}

{kind=link}